What’s the Article About? Many borrowers make seemingly safe choices when taking a home loan, but these decisions can lead to higher costs and missed opportunities. This guide explains such common mistakes and how to avoid them.

The most dangerous home loan decisions are often the ones that feel the safest! Applying for a house loan is definitely the most vulnerable point in life. You hope that everything goes safely, the process, the sanction, and the other thousand thoughts that are going on in your mind, etc. Playing safe can help, but overdoing that can prove otherwise. Why and how? Let’s see.

Although it is a tendency to look for stability, avoid risks, and stick to what seems trustworthy and reliable, here’s what you might’ve been neglecting. In the name of ‘safe choices,’ those might actually be working against you in the long run. From opting for the wrong structure to delaying decisions in the name of safekeeping, such habits can increase your financial stress or limit your flexibility. So, if you are planning to apply for a loan or have already applied for one, it’s worth your time and money to understand that some decisions that you think can protect you may actually go haywire.

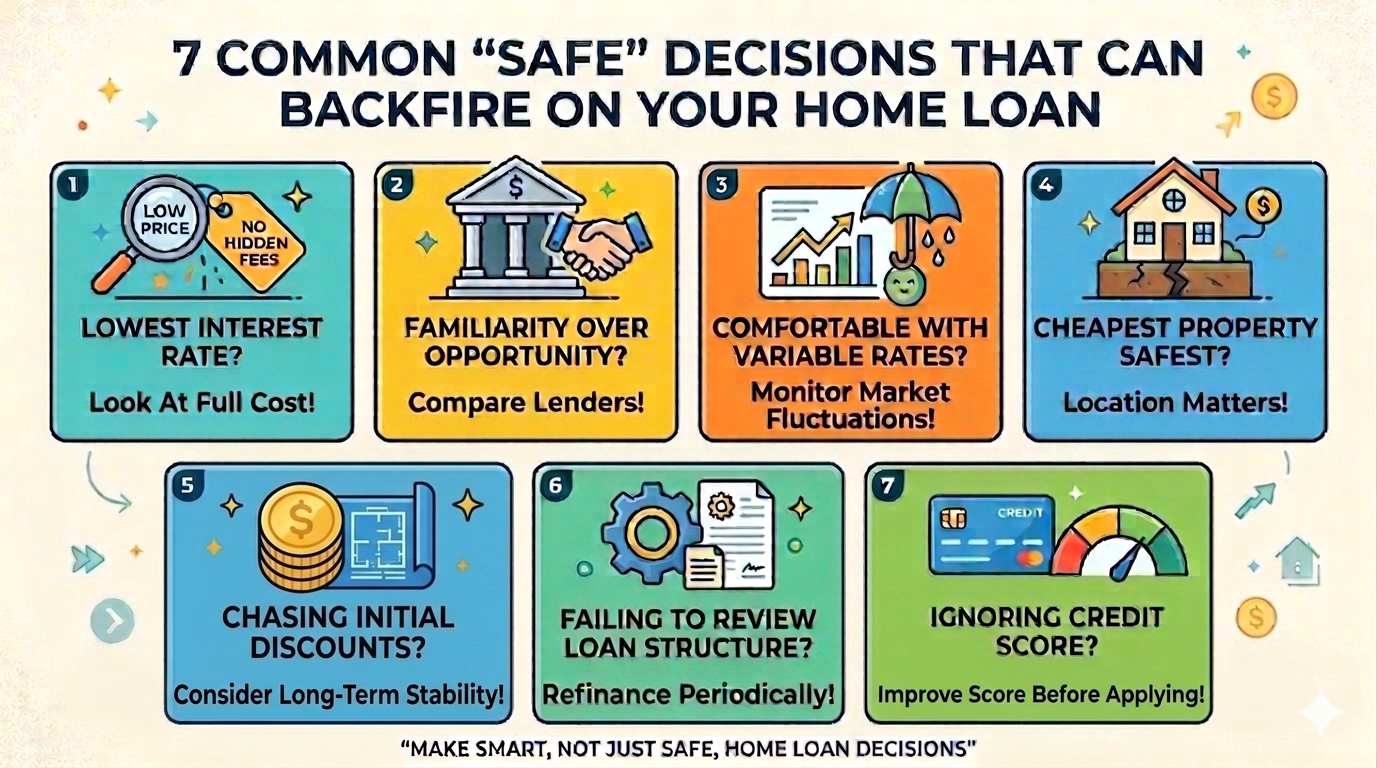

Choosing The Lowest Interest Rate Without Looking At The Full Cost.

It’s normal to hunt for the cheapest interest rate home loan. No wonder that every borrower wants to pay lower rates, EMIs, and overall costs. But here’s the catch. Focusing only on lower home loan interest rates can come with a trap, i.e., not evaluating the whole cost that is to be incurred. Some lenders offer lower interest rates, but they may include higher processing fees, stricter repayment terms, and limited flexibility when it comes to restructuring your loan.

Therefore, the best home loan interest rates aren’t really about being the lowest but about being transparent, consistent, and aligned with your long-term financial goals.

Prioritizing Familiarity Over Better Opportunities?

There are many borrowers out there who like to take a house loan from their existing bank. Reason being an established relationship and trust. Although comfortable, this does not prove otherwise. At times, your existing bank might not be providing the best home loan interest rates in comparison with others. And the bank doesn’t need to.

By not exploring other feasible and good lenders, you might miss a big opportunity to save on deals. Even a mere difference of, say, 0.5% in interest rate can lead to an increase or decrease in your EMI, resulting in a gain or loss over the loan tenure that you’ve opted for.

This is the reason why you must compare home loan interest rates across a fair number of institutions before making a final decision. Sticking with what you feel is safe can sometimes backfire on your financial interests and goals.

Being Comfortable With Introductory Or Variable Rates!!

Honeymoon interest rates can be as appealing as a sunny day, but little do we realize that once EMI calculations begin to vary, the phase goes like the wind. They offer a house loan with the lowest interest rate, making EMIs comfortable for your house loan. But once that period is over, the interest rates depend on the market conditions, further increasing or decreasing your EMI uniformity. Sometimes it leads to a much higher amount, which can also disrupt your monthly budget if you’re not prepared.

Although variable rates aren’t really bad, relying on such a discontinuity can be risky. That’s why it is highly recommended to look for revised rates on sites like Loan Bazaar and assess how they’ve performed historically. And instead of focusing on one short-term benefit, do not give up the long-term affordability for a sigh of relief.

Assuming that the cheapest property is the safest investment…

Many borrowers intend to buy a property that’s both budget-friendly and good enough to make means. Although it might seem like a responsible financial decision, choosing the cheapest option isn’t always the smartest move. You might get an affordable property with lower interest rates and lower EMIs, but such localities can come with some disadvantages. Limited infrastructure, weaker connectivity, and slower development are some common problems that are faced. This can affect not only the standard of living and the overall experience but also the property’s future value.

So, instead of just focusing on the price, you must also consider other factors, including location, accessibility, and long-term appreciation when buying a home. A slightly higher investment can prove to be the gold standard rather than second-guessing.

Waiting Too Long To Build The Perfect Down Payment!

There’s a common belief in the house loan segment. “You must save at least 20% of the property value before taking the loan.” This is because your borrowing amount is reduced, and you don’t have to bear the whole amount in one go. But waiting for too long can have unintended consequences. Real estate prices fluctuate; therefore, while you’re saving for a larger down payment, the cost of your desired property may increase at the same time. Similarly, with home loan interest rates constantly changing, the best ones might not be available today, but tomorrow. Any delay can lead to missing out on favorable conditions.

Therefore, instead of waiting for too long, aim for balance. Evaluate your financial readiness, explore options, and consider entering the market at the right time. And to reduce some burden, you can always ask your lender if they approve of the prepayment options.

Failing To Review Your Loan Structure?

Once the loan is approved, many borrowers think that their job is done! They’ll just pay the EMIs timely and be out of the spiral in the stipulated time. But a house loan isn’t really something you can forget after signing the papers. When market conditions change, and you get the opportunity to shift to a better and cheapest interest rate home loan, you’ll miss out if you don’t keep a watch on these things.

But if you incorporate the new systems in your house loan, you’ll not only improve your financial situation but also have the opportunity to restructure your loan, increase EMIs, and reduce loan tenure. Therefore, make it a habit of reviewing your loan periodically to not miss out on things that can prove to be saving lakhs for you.

Ignoring Your Credit Score Before Applying

Many borrowers assume that their financial track record is enough or spot on to consider a second time, but here’s what they can be overconfident about. Skipping a credit score check can silently weaken your loan application. Lenders rely heavily on this number to assess risk, and even a small neglect can impact your approval or interest rate.

To avoid higher interest rates despite stable income, increased chances of rejection or delays, reduced negotiation power with lenders, and missing the opportunity to improve your score beforehand, you can always keep a steady check on that 3-digit number or suffer a significant ignorance cost.

The Bottom Line

So, when it comes to ‘safe decisions,’ they can create a risk sometimes that is hidden and can prove otherwise. Whether you’re chasing the house loan with the lowest interest rate or sticking to the familiar bank for trust and advice, you might be missing out on something very important. Something that can release your financial burden over time.

Therefore, always compare home loan interest rates carefully with Loan Bazaar and evaluate your cost of borrowing and managing the loan. Because in the end, the smartest decision isn’t the one that feels the safest but the one that continues to work in your favor for the years to come.

So, before you sign that loan agreement, let us help you uncover what it could truly cost you in the long run.